Author: Mária Širaňová

Date: 18-02-2026

Cross-border trade in services has been a smaller, often neglected, brother of the international trade in goods. Yet, while the trade in goods has been severely affected by the recent episodes of COVID-induced global value chain disruptions and is under constant threat from potential tariff wars, the global trade in services is showing of a speedy recovery to pre-pandemic growth trend. The value of services exports as a percentage of world GDP reached almost 7.5% in 2023 (BiTS database, Li et al., 2025). Among them, the proportion of financial, insurance, information and intellectual property services has increased by almost seven percent since 2005, and now accounts for more than one fourth of all services traded globally (BiTS database). The services may play a dual role in their relationship to the issue of illicit financial flows.

On the one hand, several recent scandals involving cross-border VAT fraud in the European Union (see, for example, the most recent Calypso operation) have demonstrated the role of services that can serve as a complement to cross-border illicit trade. Tax and law firms with highly skilled tax advisers and lawyers can provide guidance to criminal network representatives on how to navigate the complex structure of the domestic and international tax systems. Accountants can help to keep track of the flow of illicit capital hidden within official accounting figures. Transport companies may help to disguise the illicit nature of goods being smuggled across borders.

On the other hand, the services themselves may be used to conceal the illicit nature of international capital flows. Not only may the misreporting of the value of traded services face fewer complications due to inconsistent pricing and difficulties in overall measurement (Tiwari et al., 2025), but their non-physical nature also allows them to be created ‘out of thin air’, if desired. Valuable consultancy services may be provided to launder capital that is illicit at its source (Naheem, 2015; Teichmann, 2019). While financial services intermediated by banks and other non-bank financial intermediaries are legal, they may be offered to individuals with illicit incentives. These services are often provided in tax havens and financial centers, which are considered more susceptible to money laundering (Blum et al., 1998; Tavares, 2013), as demonstrated by the Panama Papers scandal and others like it.

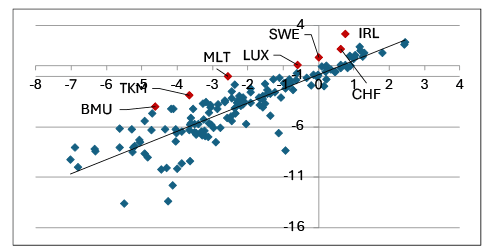

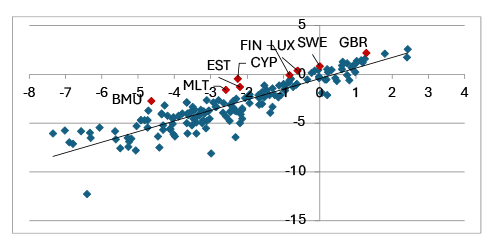

To illustrate the interconnected nature of cross-border trade in goods and services, we examine data on misreported export values between Greece and its main European trading partners in 2023. A recent investigation by the European Anti-Fraud Office uncovered a long-running fraudulent scheme involving the shipment of misreported Chinese goods via the Greek port of Piraeus to other European Union member states. First, we identify financial centers as economies with an disproportionate share of earnings from cross-border trade in financial services compared to their level of global trade involvement (Figure 1a), using the newly released BiTS data. For comparison purposes, we also identify economies that serve as global hubs for intellectual property-related fees and services (Figure 2a) and information technology services (Figure 3a).

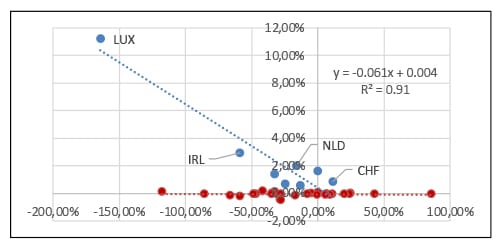

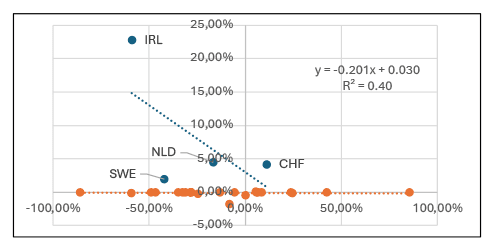

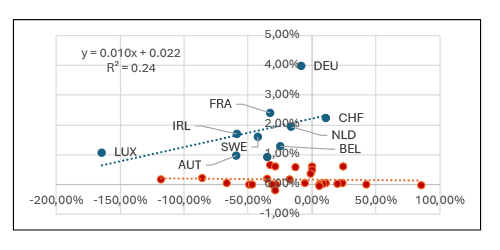

Next, we plot the calculated index of excess proceeds in three service sectors against the export misreporting measure for Greek trading partners (see Figures 1b–3b). For the top eight economies that derive a substantial income from the financial services sector internationally, the negative association is rather pronounced, with Luxembourg being an important driver of the empirically observed correlation. Unproportional payments for intellectual properties are strongly concentrated in a few selected economies, and their link to export misreporting seems to be less robust. By contrast, only very weak positive evidence was observed between economies characterized by a larger role for cross-border income from information services and the extent of export misreporting practices in Greece.

This simple exercise demonstrates that economies with a strong international financial services sector may attract individuals with illicit intentions, and vice versa. This may be less prominent in other service sectors. Further research into the complex nature of the interlinkages between the illicit trade of goods and services could therefore help to uncover the potential actors, intermediaries, channels and tools involved in illicit international practices.

- Figure 1: 1 a) Global share on cross-border financial services inflows (logs, y-axis) vs. global share on cross-border trade in goods (logs, x-axis)

- 1 b) Excess share on global cross-border financial services inflows (diff, y-axis) vs. export misreporting of Greek trade partners (%, x-axis)

- Figure 2: 2a) Global share on cross-border intellectual property services inflows (logs, y-axis) vs. global share on cross-border trade in goods (logs, x-axis)

- 2 b) Excess share on global cross-border intellectual property services inflows (diff, y-axis) vs. export misreporting of Greek trade partners (%, x-axis)

- Figure 3: 3 a) Global share on cross-border information technology services inflows (logs, y-axis) vs. global share on cross-border trade in goods (logs, x-axis)

- 3 b) Excess share on global cross-border information technology services inflows (diff, y-axis) vs. export misreporting of Greek trade partners (%, x-axis)

References:

Nan Li, Sergii Meleshchuk, Qiuyan Yin, Dennis Zhao, and Robert Zymek, 2025, Bilateral Trade in Services: Insights from A New Research Dataset, International Monetary Fund, WP/25/163

Milind Tiwari, Jamie Ferrill and Douglas M.C. Allan, 2025, Trade-based money laundering: a systematic literature review, Journal of Accounting Literature, 47 (5), pp. 1-26

Naheem, M. A. 2015. Trade based money laundering: towards a working definition for the banking sector, Journal of Money Laundering Control, 18(4), pp. 513-524.

Teichmann, F. M. J. 2019. Money laundering and terrorism financing through consulting companies, Journal of Money Laundering Control, 22(1), pp. 32-37.

Jack A. Blum, Michael Levi, R. Thomas Naylor, Phil Williams, 1998, Financial Havens, Banking Secrecy and Money Laundering, United Nations Office for Drug Control and Crime Prevention.

Tavares, R. 2013. Relationship between Money Laundering, Tax Evasion and Tax Havens, Thematic Paper on Money Laundering, European Parliament: Special Committee on Organised Crime, Corruption and Money Laundering (CRIM) 2012-2013